Compound fracturing

Max Lawson on how overlapping global crises are deepening inequality, entrenching poverty, and accelerating the concentration of wealth and power.

When the economic shock to the global economy hit with the formal announcement of the Covid-19 pandemic in March of 2020, we had to look all the way back to 2008 for inspiration. Fortunately, at Oxfam there were a handful of very old people still doddering around who remembered those days. Don’t get me wrong, the 2010’s had been pretty lacklustre in terms of poverty reduction, and full of nasty austerity for ordinary people and rapidly growing wealth for billionaires, but we had nevertheless not had a really global level economic shock for over a decade.

Now, sitting here in 2026, this feels mercifully calm. By my count, since 2020 we have had five global level shocks to the economic system. First was the impact of Covid itself on the global economy.

Second was the credit crunch that followed the pandemic as rich countries rapidly increased interest rates prompting further debt crises. Virtually simultaneous with this was the energy and food crisis that hit the globe after the Ukraine War. Fourth was the widespread economic disruption prompted by the actions of the second Trump administration; the sudden imposition of tariffs on the majority of countries, and the huge cuts to Official Development Assistance (ODA) that happened pretty much simultaneously. Now fifth is unlawful US and Israel war against Iran, which is creating a food and energy shock that may dwarf that of the Ukraine War.

Add to this a sixth crisis too, which was already becoming apparent in the 2010’s but seems much more present in the 2020’s. The relentless rise in huge and horrific extreme weather events and the slow but equally relentless reductions in food production because of climate breakdown.

All in all, the 2020’s have so far been a decade of almost permanent economic crisis.

Winners, losers and inequality in times of crisis

Each of these crises has its own unique aspects but also has some strong similarities, especially regarding inequality. These crises are always hardest on ordinary people everywhere; and particularly on women, racialised groups and other vulnerable people. They are also particularly hard on ordinary people in the Global South, in countries that are largely unable to provide them the kind of social protection that is available to many in the Global North.

Each crisis costs governments dearly, and drives up public debt, as they seek to stay afloat and where possible help their populations. Once again, whilst almost all governments feel the fiscal pain, rich country governments, with their hard currencies, have much lower borrowing costs, and Global South governments are the most exposed.

Finally, each crisis, whilst at times temporarily denuding the fortunes of the richest, always seems to leave them richer than they were before.

Compound crises

Picture a family in Nairobi, whose main breadwinner is a taxi driver, who have a small plot of land back in their home village. The lockdowns of Covid-19 hit business hard with tourism grinding to a halt, but they managed to scrape by. Poor and erratic rains have meant food and income from their small piece of land has been much lower than it used to be. At one point in 2021 they had to move house in their informal settlement of Kawangware in Nairobi because of flooding that damaged their building and swept away many of their belongings.

When the food and fuel crisis hit in 2022 they had to take out a loan against their car, so they managed to avoid selling the taxi but ended up in much more debt. In 2023 the hospital bills and funeral costs of the taxi drivers’ mother also added significantly to their financial problems. Their oldest daughter had to drop out of high school as there was not enough money to pay school fees.

Now in 2026, with the very sharp rise in food and fuel prices once again, they may be forced to sell the taxi, to have enough to pay rent and buy food to survive. They are contemplating taking their other children out of school and moving back to the village.

This is a fictional story but based on a family I know very well. It is I think probably very typical of the majority of humanity- around half of the global population live below the $8.30 a day poverty line. Not the poorest of the poor but just scraping by. It shows how personal and global shocks hit families hard, and how they can also interact. How it is possible to get through one crisis, maybe two, but beyond that crises compound and the scars left become more and more permanent and serious. This includes debt traps and the slow depletion of what few assets a family owns, including the need to sell assets like a car that undermine the way the family makes its money.

This is known as the ‘poverty rachet’ effect, made famous by the brilliant Robert Chambers; whereby sudden, irreversible events (like a medical emergency, a bad harvest, or a forced distress sale of land) can permanently lock a household into a lower economic tier.

Governments too, follow a similar path, having to take on further debts, often in foreign currency and at high interest, to get through one crisis, only to be hit by another, and then another, slowing development to a standstill and throwing things into reverse.

Wealth rachets

Whilst not described perhaps in quite the same way, wealth too is I think subject to a rachet effect from multiple crises. We know of course that in normal times, when someone becomes very wealthy, then that wealth can develop a momentum of its own. Wealth begets more wealth and is maintained over generations.

At times of crisis economic wealth is often in part destroyed, but what we see is how fast it bounces back, and how resilient it is. Wealth can become more concentrated still, as even when the richest lose assets in a crisis, they still have resources left to buy up the assets sold by others, often at knockdown prices, or are able to use their wealth to lend to others, often through financial intermediaries. So, each crisis can increase wealth concentration sharply.

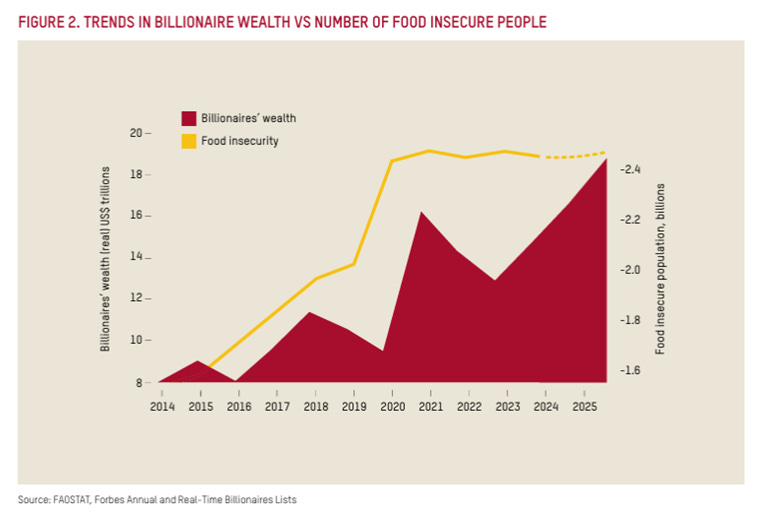

The super rich saw their wealth hugely inflated by government interventions in their economies in response to the 2008 Financial Crisis and then again in 2020 when Covid-19 hit; trillions of dollars were poured into the global economy, driving up asset prices worldwide, and with this the fortunes of the richest. They have been able to use these resources to reinvest and in turn to make money out of subsequent crises; for example, in lending more money at high rates of interest to countries of the Global South, or in the rapidly rising shares of food and energy corporations or weapons manufacturers.

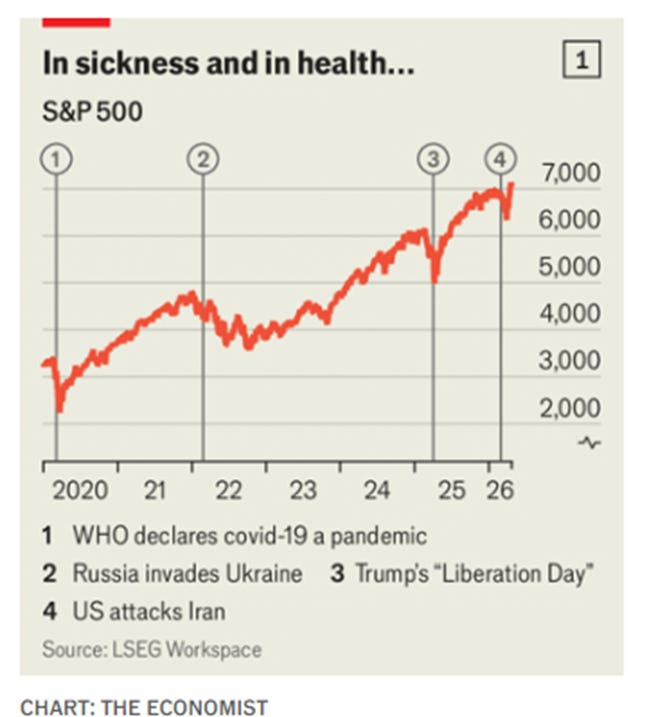

This graph in The Economist a couple of weeks ago pretty much sums that up:

Centrifugal or centripetal crises

Joseph Stiglitz talks about centrifugal forces in the economy, which, like a roundabout in children’s playground, force things outwards, driving inequality higher. Economic shocks are I think very likely to have this centrifugal impact on our economies, with each crisis driving us further apart.

He contrasts this with centripetal forces in the economy, which can act to increase equality. An example could be market regulation, or investment in public services.

Yet in the 20th century, the response to shocks like the Great Depression in the USA, or World War Two, actually led to greater equality, not greater inequality in many countries. There is no automatic link between economic crises and rising inequality, although this is much more common. Governments can respond to economic shocks ways that actually reduce equality.

Most recently this was true with income inequality during Covid-19 in a number of countries; in the USA, whist wealth inequality grew, income inequality fell faster during Covid-19 than it had for decades, and child poverty was cut by 40%, the largest drop ever recorded, thanks to the prompt and generous action by government. Sadly, these government actions were allowed to expire soon afterwards in Congress, losing that progress that was made against child poverty.

At times of crisis, the way people respond often shows their true colours- this is true of governments too.

Equality is also the best protection

Looking at things the other way round, in a world of almost annual economic shocks and seemingly permanent crisis I strongly think that the most direct way to mitigate their harmful impacts is to have a low level of inequality in the first place.

More equal societies for a start radically reduce the individual impact of personal crises. For example, free, universal public healthcare stops anyone being forced into poverty by catastrophic health expenditures. It spreads the risk, and makes individual lives far less precarious, even if their incomes are still not very high.

Equality also helps mitigate the impact of global crises too. More equal societies are more cohesive. Risks are distributed more fairly across society, and as a result the overall risks faced are reduced. They are more prepared to cope with shocks when they arrive, whatever those shocks are; be it the impact of AI, rogue presidents, typhoons, wars, or whatever else.

Equality is the best protection.

ENDS

Author: Max Lawson, Head of Inequality Policy at Oxfam International and EQUALS podcast co-host. He is also a visiting Professor in Practice at the LSE International Inequalities Institute and the co-chair of the Global People’s Medicines Alliance.

In our previous EQUALS episode, Adam Hanieh explores how crises like war, financial shocks, and pandemics ripple across borders through energy prices, food systems, and rising living costs, hitting the poorest of the population the hardest. Listen here.

War, Oil, and Inequality: Who Wins and Who Loses

In this episode, Adam Hanieh explains why crises like war, financial shocks, and pandemics don’t stay where they start. They move through the structures of the global economy.